Corbis Intelligence

Research and Insights

Commercial real estate intelligence grounded in academic research, real economic data, and the agent systems behind Corbis and EQUIRE.

Search articles by title, content, or tags...

Commercial real estate intelligence grounded in academic research, real economic data, and the agent systems behind Corbis and EQUIRE.

Agentic Assets Research Team

Corbis Research

February 26, 2026

8 min read read

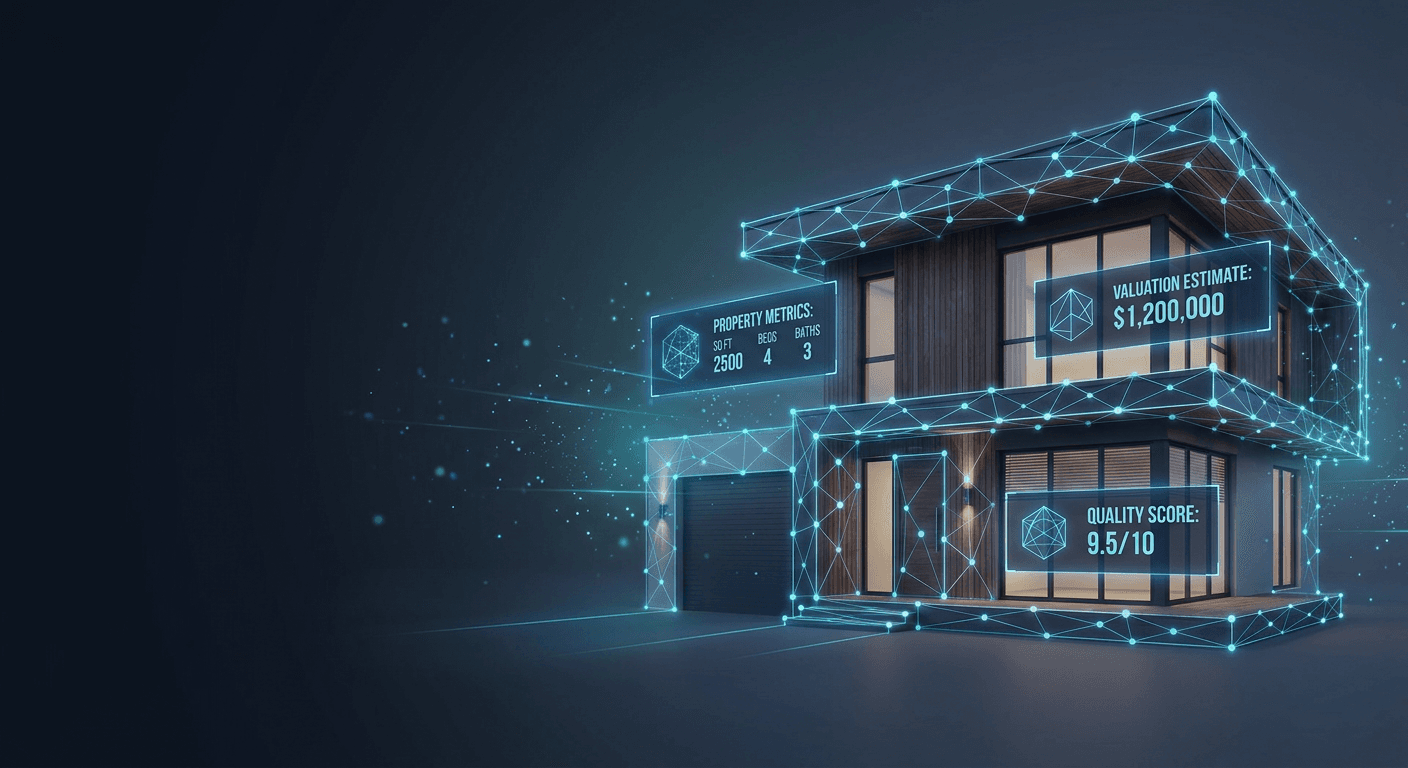

The loud version of AI in real estate valuation is easy to picture: a model estimates a property value from photos, parcel data, rent comps, and market history. The quieter version may matter more. Valuation is becoming more structured before it becomes more autonomous. The Uniform Appraisal Dataset modernization effort, summarized by Fannie Mae through its UAD program materials, pushes appraisal reporting toward standardized fields, controlled definitions, and machine-readable delivery.

That matters for AI because models do not improve only when architectures improve. They improve when the inputs become consistent enough to compare, validate, and monitor. A narrative PDF is hard to audit at scale. A structured field that records condition, quality, location influence, comparable adjustments, and appraiser rationale can be tested across time and geography.

Academic work already points in this direction. Yazdani and Raissi's self-supervised vision transformer work on property valuation shows how visual information can be combined with tabular housing attributes. Teikari, Jarrell, Azh, and Pesola's Architecture of Trust paper argues that AI-augmented valuation requires more than predictive accuracy. It needs human oversight, uncertainty reporting, fairness controls, and domain-specific evaluation.

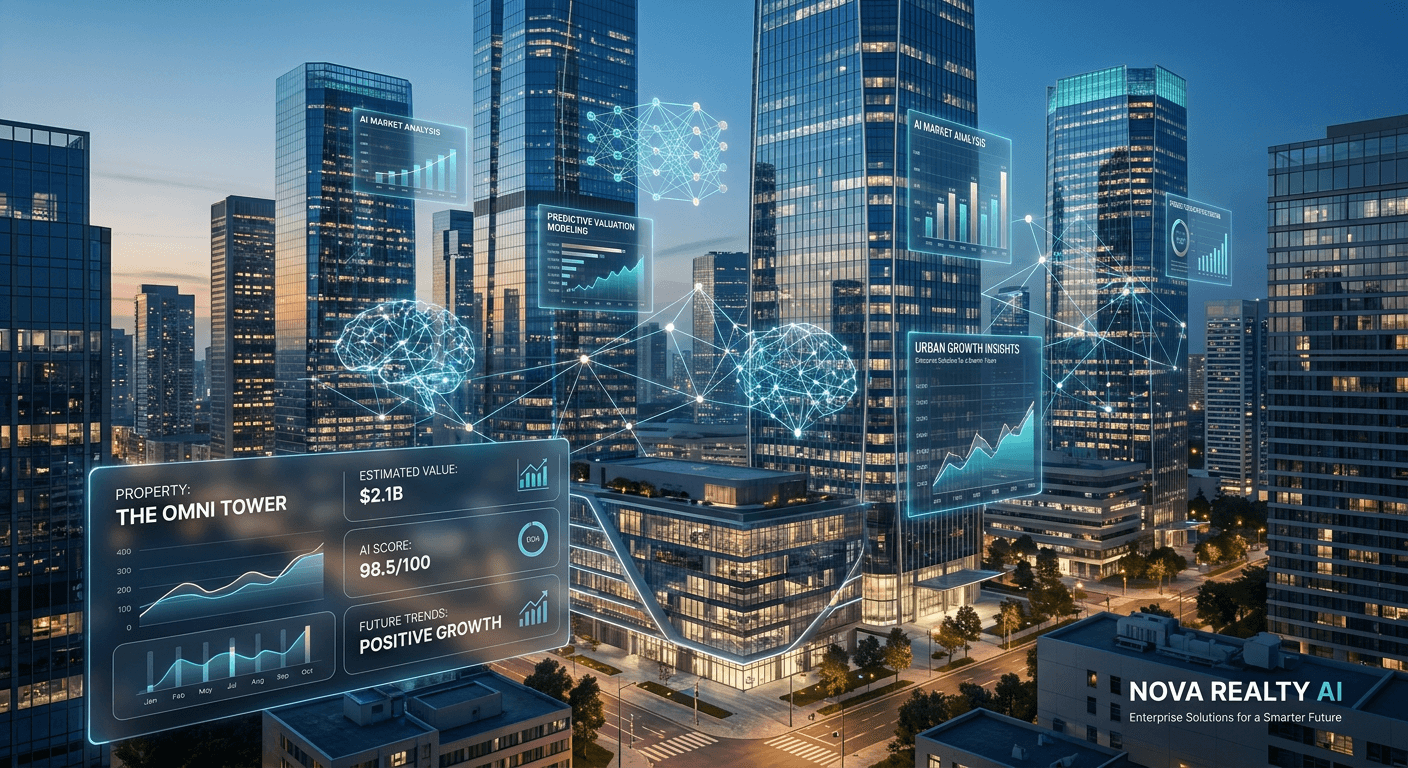

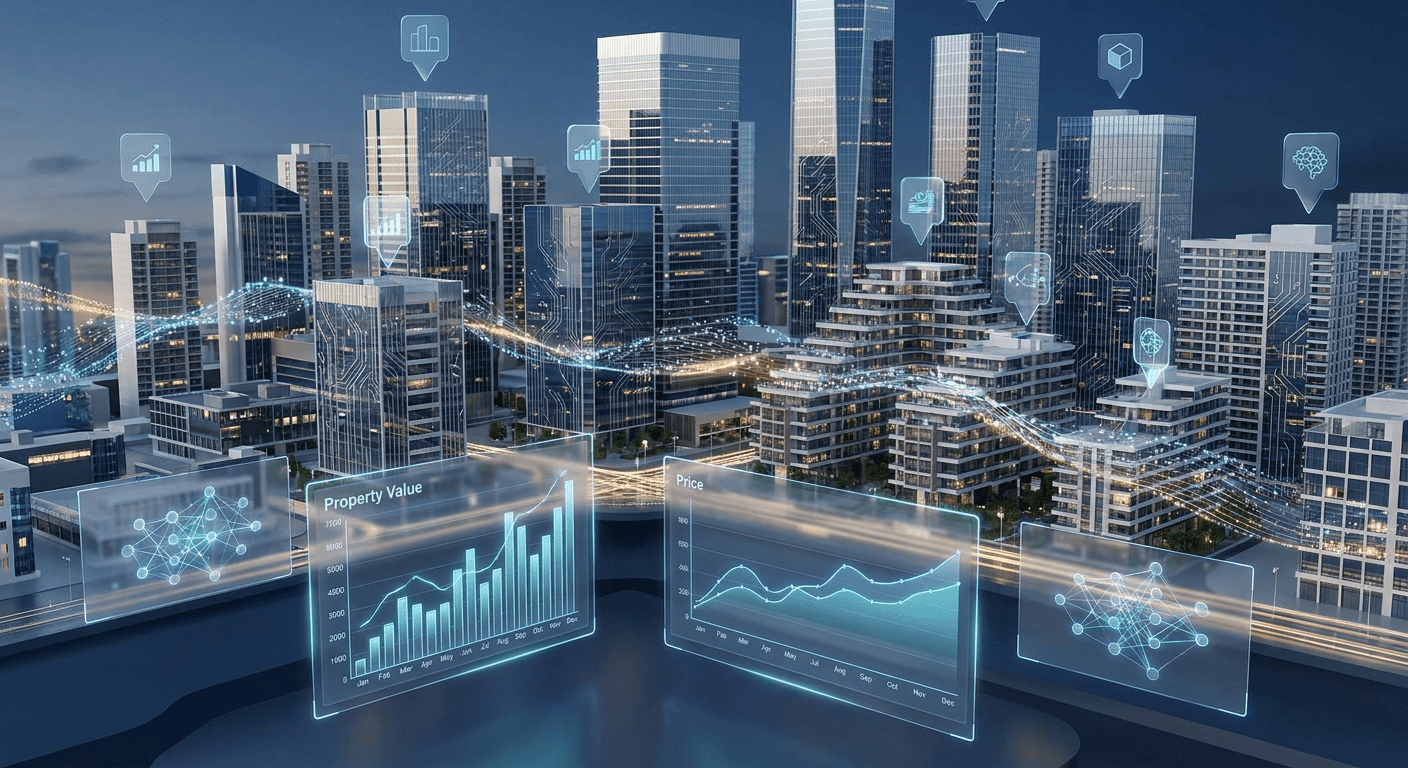

For commercial real estate, the same principle applies even when the asset class differs. A model can identify patterns in rent growth, location, tenant exposure, cap rates, expenses, or capital expenditures. But if source fields are inconsistent, stale, or selectively reported, the model simply becomes a faster way to amplify bad inputs.

The long-run opportunity is not a black-box value button. It is an evidence file that connects each valuation claim to structured inputs, source documents, market benchmarks, and model assumptions. An appraiser or analyst can still make a judgment call, but the judgment becomes easier to review. Which comps were excluded? Which adjustment drove the conclusion? Which rent assumption changed since the prior valuation? Which photo evidence supports the condition rating?

That is also where AI can create better internal controls. A valuation platform can flag when one appraiser consistently adjusts above peers, when an expense assumption breaks from the market, or when a condition score conflicts with image evidence. Those checks do not remove professional judgment. They make professional judgment observable.

The risk is that structured fields make outputs look more certain than they are. Real estate markets are thin, local, and slow to reveal information. Commercial assets are especially heterogeneous. A model trained on the most visible data may miss negotiated concessions, tenant credit deterioration, capex needs, or local political constraints.

That is why the February 2026 valuation story should not be framed as appraisers versus AI. The better framing is structured evidence versus opaque narrative. AI can help if it turns valuation into a more inspectable process. It can harm if it turns weak inputs into confident numbers. The next generation of valuation tools should therefore be judged less by whether they produce a price and more by whether they can show how that price was built.

Commercial valuation has more heterogeneity than conforming residential appraisal, but the same lesson travels well. Cap rates, tenant credit, lease structures, concessions, capital expenditure needs, and market rent assumptions are often described in prose or scattered across files. If those inputs are not structured, AI has to infer them from messy documents. That raises cost and error risk. If they are structured, the system can compare assets, explain adjustments, and show where human judgment changed the model output.

The FHFA working paper on AI and mortgage lending is useful here because it treats AI as a governance and data-quality issue, not only a prediction issue. The same stance should guide CRE. Better models do not remove the need to document why a comparable was included, why a rent premium was applied, or why a stabilized margin is credible.

The winning valuation workflow will probably look less like an automated price oracle and more like an evidence graph. The model proposes, but the file explains.

Discover how purpose-built LLMs like Real-GPT are revolutionizing property valuation, investment analysis, and compliance in real estate through explainable AI and advanced automation.

Discover how AI computer vision is revolutionizing property assessment with 18-20% error reduction and $68,000 higher valuations, transforming real estate through automated analysis.

Discover how AI is revolutionizing real estate with a projected $41.5B market by 2033. From automated valuations achieving 2-4% accuracy to property management cost cuts of 18-30%, learn the tools and strategies transforming the industry.